- Categories:

How to Proceed With COVID-19 Financial Assistance

- By Molly Bond

The CARES Act, signed into law on March 27, has provided $659 billion (as of June 2020) in relief funding for small businesses and contains a number of provisions to help streamline the loan process and put grants and forgivable loans into the hands of small business owners. August 8, 2020, is the last day a new loan can be approved.

Booksellers in need of capital should start the loan process now by first gathering the necessary documentation and then making a determination as to what loan or loans are most appropriate for their needs. The first step for any store that will be filing an application for an Economic Injury Disaster Loan (EIDL)/grant or an SBA-approved loan is to compile all the necessary documentation. (Here’s more information on what you’ll need.)

Booksellers in need of capital should start the loan process now by first gathering the necessary documentation and then making a determination as to what loan or loans are most appropriate for their needs. The first step for any store that will be filing an application for an Economic Injury Disaster Loan (EIDL)/grant or an SBA-approved loan is to compile all the necessary documentation. (Here’s more information on what you’ll need.)

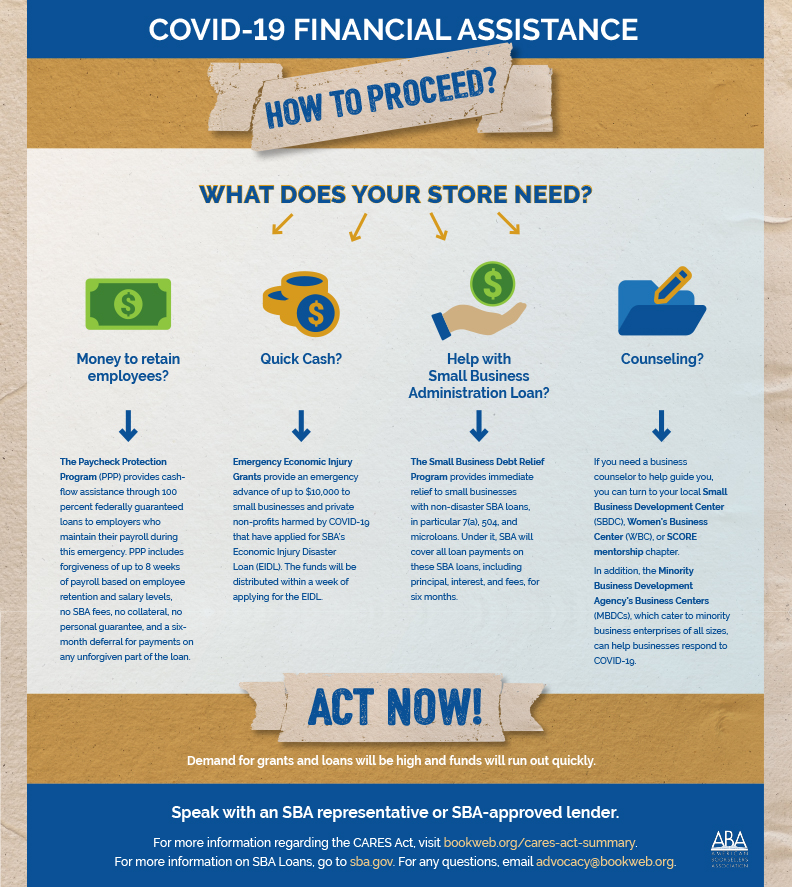

What you need to know: Act fast because demand for grants and loans will be high and funds will run out quickly.

The question for every bookseller is, should they apply for a grant, a forgivable loan, or both? The following questions and the information below can help point booksellers in the right direction. (As always, we encourage booksellers to speak with an SBA representative or SBA-approved lender before finalizing their decision.)

What does your store need?

- Money for payroll to retain employees? The Paycheck Protection Program might be right for you.

- Quick cash? Look into the SBA’s Emergency Economic Injury Disaster Loan (EIDL) Grant.

- Help on your current or potential SBA Loan? Check out the Small Business Debt Relief Program.

- Counseling? SBA’s resource partners might be your best bet.

For a more detailed summary of the CARES Act, see ABA’s summary for members, the small business owner’s FAQ guide, and the PPP information sheet for borrowers.

1. Paycheck Protection Program: Money for payroll

The Paycheck Protection Program (PPP) provides cash-flow assistance through 100 percent federally guaranteed loans to employers who maintain their payroll during this emergency. PPP includes forgiveness of up to 8 weeks of payroll based on employee retention and salary levels, no SBA fees, no collateral, no personal guarantee, and a deferral for payments on any unforgiven part of the loan.

Eligibility: Businesses, nonprofits, Tribal businesses, sole proprietorships, self-employed individuals, and independent contractors with less than 500 employees can apply for a PPP loan.

Maximum loan amount: $10 million. Your loan amount will be equal to 2.5 times your average monthly payroll costs (see below for eligible payroll costs). See how to calculate your maximum loan amount by business type, including self-employed with and without employees, partnerships, S and C corporations, etc.

Covered loan period: February 15, 2020–December 31, 2020

Interest rate (for non-forgivable uses): If the funds are used for non-forgivable expenses, there is a 1 percent fixed rate. Payments of principal and interest on the loan are deferred until the date loan forgiveness is remitted to the lender. For borrowers who do not apply for forgiveness, payment will not begin until 10 months after the last day of the covered period. However, interest will accrue over this period. For any portion of a PPP loan that is not forgiven, the loan term was originally two years. However, the PPP Flexibility Act passed in June 2020 changed the minimum loan term to five years for new loans. The PPP Flexibility Act does allow lenders and borrowers with pre-existing loans to mutually agree to modify the loan term to five years. Talk to your lender for more information.

Forgivable expenses: (1) Eligible payroll costs; (2) interest on mortgages incurred before February 15, 2020; (3) rent under a lease that began before February 15, 2020; and (4) covered utilities for service that began before February 15, 2020.

Eligible payroll costs: (1) Salary, wages, commissions, or tips (capped at $100,000 on an annualized basis per employee); (2) payment for vacation, parental, family, medical, or sick leave (not including costs for mandated paid leave under the Families First law); (3) allowance for dismissal or separation; (4) payment for group health care benefits; (5) payment of retirement benefits; (6) payment of state or local tax.

Conditions for loan forgiveness: The loan amount will be forgiven in full if the funds are used to cover eligible payroll expenses, mortgage interest, rent, and utility costs and employee and compensation levels are maintained. Borrowers seeking loan forgiveness must use at least 60 percent of the loan on payroll costs. According to the SBA, if a borrower uses less than 60 percent of the loan amount for payroll costs during the forgiveness covered period, the borrower will continue to be eligible for partial loan forgiveness, subject to at least 60 percent of the loan forgiveness amount having been used for payroll costs. For more information, see PPP Loan Forgiveness Information.

Rehired employees: You have until December 31, 2020, to restore your full-time employment and salary levels.

Distribution of funds: Loans will be distributed by any SBA-approved lender or through participating federally insured depository institutions, federally insured credit unions, and Farm Credit System institutions. Other regulators will be available once approved and enrolled. Consult with your local lender to see if it is participating. Find an eligible lender near you.

Necessary documentation: Average monthly payroll, payroll documentation, number of jobs, list of all owners with a greater than 20 percent ownership stake.

Compatibility with other financial assistance: You can have both an EIDL grant (see below section) and a PPP loan as long as you do not use the funds for the same purpose. If you ultimately receive a PPP loan or refinance an EIDL into a PPP loan, any advance amount received under the Emergency Economic Injury Grant Program would be subtracted from the amount forgiven in the PPP. In other words, if your business spends 100 percent of the PPP funds (say $10,000) on forgivable expenses, but you also receive an EIDL grant (say $3,000), all $10,000 will be forgiven, but you’ll be required to pay back to $3,000 under the PPP loan terms. You can also apply for a non-disaster SBA loan in addition to a PPP loan as long as you do not use the funds for the same purpose. Debt relief offered to businesses to non-disaster loans with the SBA does not apply to PPP loans (see below section).

Apply here: Access the PPP application form here. You will need to complete and submit the PPP application with the required documentation. Small businesses and sole proprietors can apply for loans through SBA lenders starting Friday, April 3. Independent contractors and self-employed individuals can apply for loans starting Friday, April 10. **Note: speak with your SBA-approved lender first to ensure you fill out the correct application**

Additional information: For more information, visit the Treasury Department’s CARES Act page, and contact your local SBA district office, Women’s Business Center, and/or SBA-approved lender for assistance. SCORE, a resource partner of the SBA, may also be able to help.

2. Emergency Economic Injury Disaster Loan (EIDL) Grant: Quick Cash

Emergency Economic Injury Grants provide an emergency advance of up to $10,000 to small businesses and private non-profits harmed by COVID-19 that have applied for SBA’s Economic Injury Disaster Loan (EIDL). The funds will be distributed within three days of applying for the EIDL.

Eligibility: Businesses, sole proprietors, independent contractors, and cooperatives and employee owned businesses with less than 500 employees, as well as private non-profits, in all 50 states, D.C., and the territories may apply for an EIDL. The SBA will approve businesses for an EIDL loan based on: (1) the credit score of the applicant; or (2) an alternative appropriate method to determine applicant’s ability to repay. To access the up to $10,000 advance, you must first apply for an EIDL (max. loan of $2 million with interest rate of 3.75 percent for small businesses), and then request the advance.

Maximum grant amount: $10,000

Covered period: January 31, 2020–December 31, 2020

Eligible expenses: (1) Providing paid sick leave to employees unable to work due to the direct effect of COVID-19; (2) maintaining payroll to retain employees during business disruptions or substantial slowdowns; (3) meeting increased costs to obtain materials unavailable from the applicant’s original source due to interrupted supply chains; (4) making rent or mortgage payments; and (5) repaying obligations that cannot be met due to revenue losses.

Repayment: The advance does not need to be repaid. See the below section on compatibility with other financial assistance for information on how a PPP loan affects repayment.

Distribution of funds: The SBA will distribute the grant funds.

Necessary documentation: Gross revenues for the 12 months prior to January 31, 2020; cost of goods sold for 12 months prior to January 31, 2020; corporate name, ID number, and social security numbers for all owners; the date the business was established; how long the current owner has been there; names, address, phone numbers, and social security numbers for all owners; the number of employees as of January 31, 2020; and bank name, account number, and routing number.

Compatibility with other financial assistance: You can have both an EIDL grant and a PPP loan as long as you do not use the funds for the same purpose. If you ultimately receive a PPP loan or refinance an EIDL into a PPP loan, any advance amount received under the Emergency Economic Injury Grant Program would be subtracted from the amount forgiven in the PPP. In other words, if your business spends 100% of the PPP funds (say $10,000) on forgivable expenses, but you also receive an EIDL grant (say $3,000), all $10,000 will be forgiven, but you’ll be required to pay back to $3,000 under the PPP loan terms.

Apply here: Apply for the EIDL and the EIDL grant here. Remember, you must apply first for an EIDL and then request the advance grant.

Additional information: For more information, contact the SBA disaster assistance customer service center at 1-800-659-2955 or by email at [email protected].

3. Small Business Debt Relief Program: If your business has or wants an SBA Loan

The Small Business Debt Relief Program provides immediate relief to small businesses with non-disaster SBA loans, in particular 7(a), 504, and microloans. Under it, SBA will cover all loan payments on these SBA loans, including principal, interest, and fees, for six months. This relief will also be available to new borrowers who take out loans within six months of the President signing the bill into law.

This debt relief program does not apply to PPP loans since PPP loans are already eligible for loan forgiveness. You can have both a non-disaster loan and a PPP loan as long as you do not use the funds for the same purpose.

4. SBA’s Resource Partners: Get more information from the experts

If you need a business counselor to help guide you, you can turn to your local Small Business Development Center (SBDC), Women’s Business Center (WBC), or SCORE mentorship chapter.

In addition, the Minority Business Development Agency’s Business Centers (MBDCs), which cater to minority business enterprises of all sizes, can help businesses respond to COVID-19.

Additional Resources

MultiFunding offers free daily webinars explaining the small business provisions in the CARES Act. You can sign up for the webinar here. Additionally, MultiFunding has an SBA/COVID-19 forum.

Lawyers for Good Government Foundation, a non-profit network of more than 125,000 legal advocates in all 50 states, announced a nationwide COVID small business legal clinic project. If you are interested, sign up here to be notified when a clinic becomes available in your city.

Check your local government’s website for potential grants and low-interest loans. ABA has created a state-by-state resource page to help you locate this financial assistance.

Questions can be directed to [email protected].